Why has the retail sector moved into the big leagues when it comes to renewable energy procurement?

In the last article in this series, we undertook a deep-dive into the ICT industry and why it – and the growth of data centres specifically – is so significant for the development of renewable energy in Central and Southeastern Europe.

This time we will be looking at another sector – retail – which may not be able to compete with ICT in terms of the total amount of renewable electricity contracted through power purchase agreements (PPAs), but which is growing even faster. We will consider the most important factors driving that growth, and explore what the implications might be for Southeastern Europe.

1. How does retail compare with other industry sectors when it comes to renewable energy procurement?

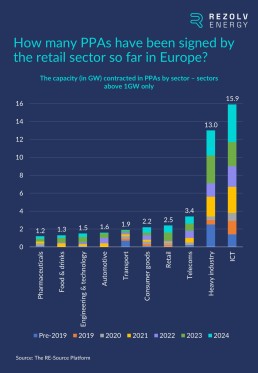

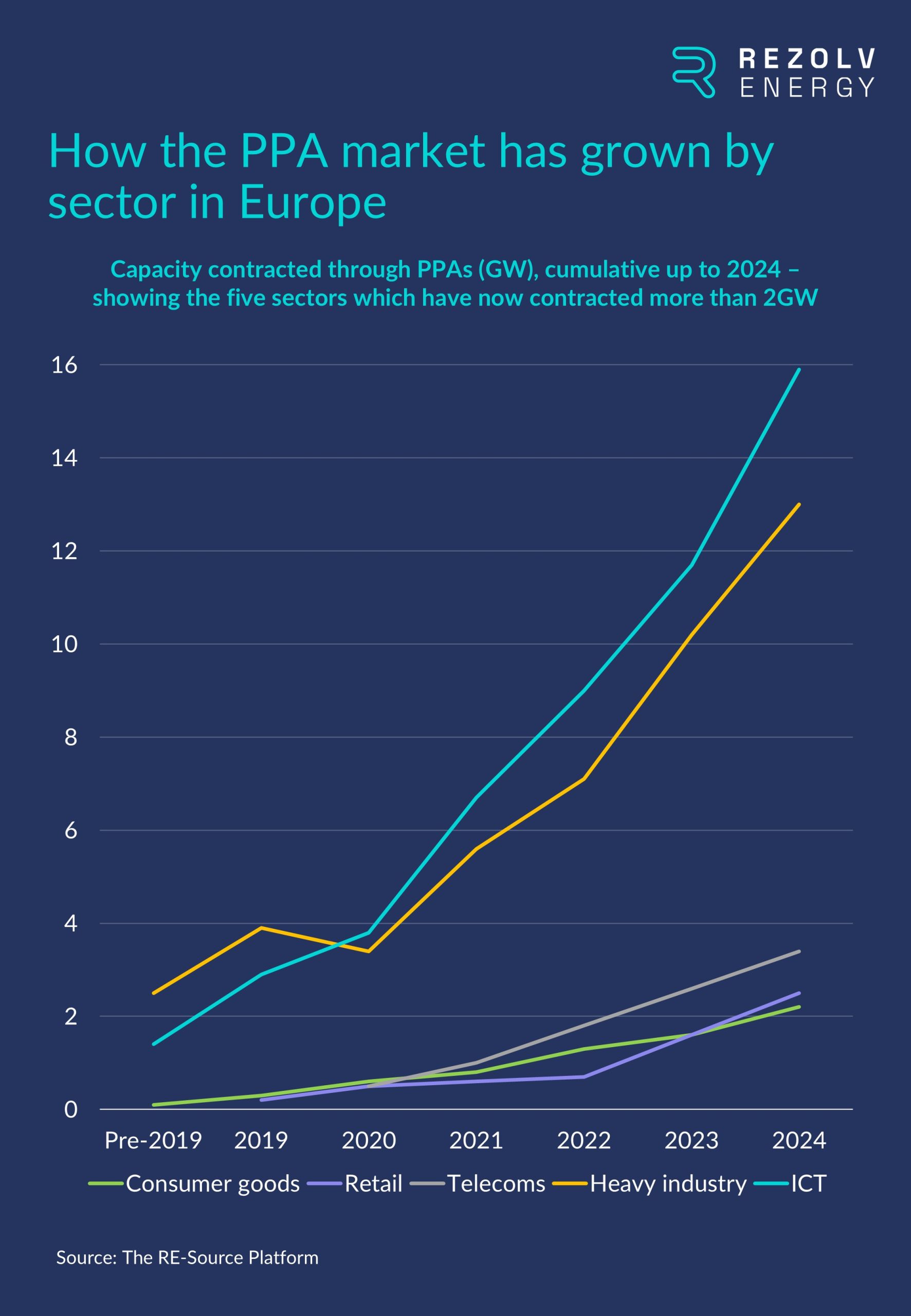

The put things into context, the retail sector currently stands fourth on the list of sectors which has contracted the most green energy through PPAs, with 2.5GW in total. There is a 0.9GW gap to the telecoms industry (a sector we explored earlier in this series) in third, and then a chasm to the two leading sectors: ICT (13GW) and heavy industry (15.9GW):

However, over the last two years, retail has been the fastest-growing sector of all, increasing contracted capacity by 257% between 2022 to 2024 (albeit from a relatively low base). In the same time period, telecoms grew by 89%, heavy industry by 83%, ICT by 77% and consumer goods by 69%:

2. Which retailers are leading the way?

The retail sector is slightly different to ICT, which is dominated by a relatively small number of big tech companies when it comes to the signing of PPA deals.

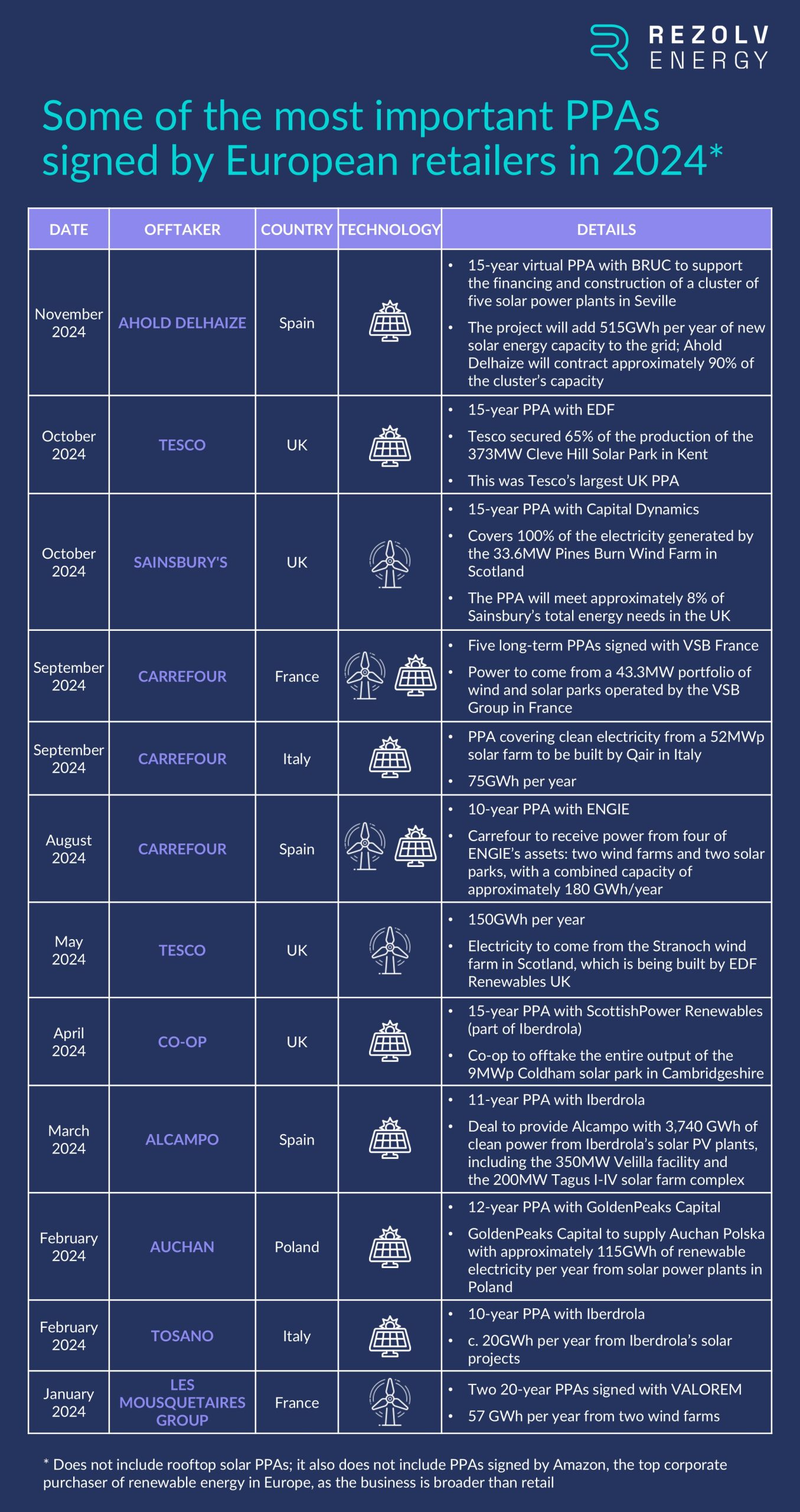

Pexapark’s ‘Renewables Market Outlook 2025’ included two retailers – Carrefour and Tesco – in its Top 10 list of corporate PPA buyers in 2024, the first time any supermarket chains had made that list. However, a quick look at the most significant retail sector PPAs in 2024 indicates that while most were signed by supermarket chains, there was a variety of companies and countries, and a good mix of both wind and solar PPAs:

3. What is driving retailers towards green PPAs?

There are four main factors driving this move towards renewable energy PPAs in the retail sector. Three of them are not specific to retail; the final one is a bigger factor in retail than in the other sectors we have explored so far in this series (automotive, telecoms and ICT).

Let’s start with the factors which are not unique to retail:

a) PPAs can reduce energy costs for electricity-intensive companies, as well as protecting them from volatile energy markets

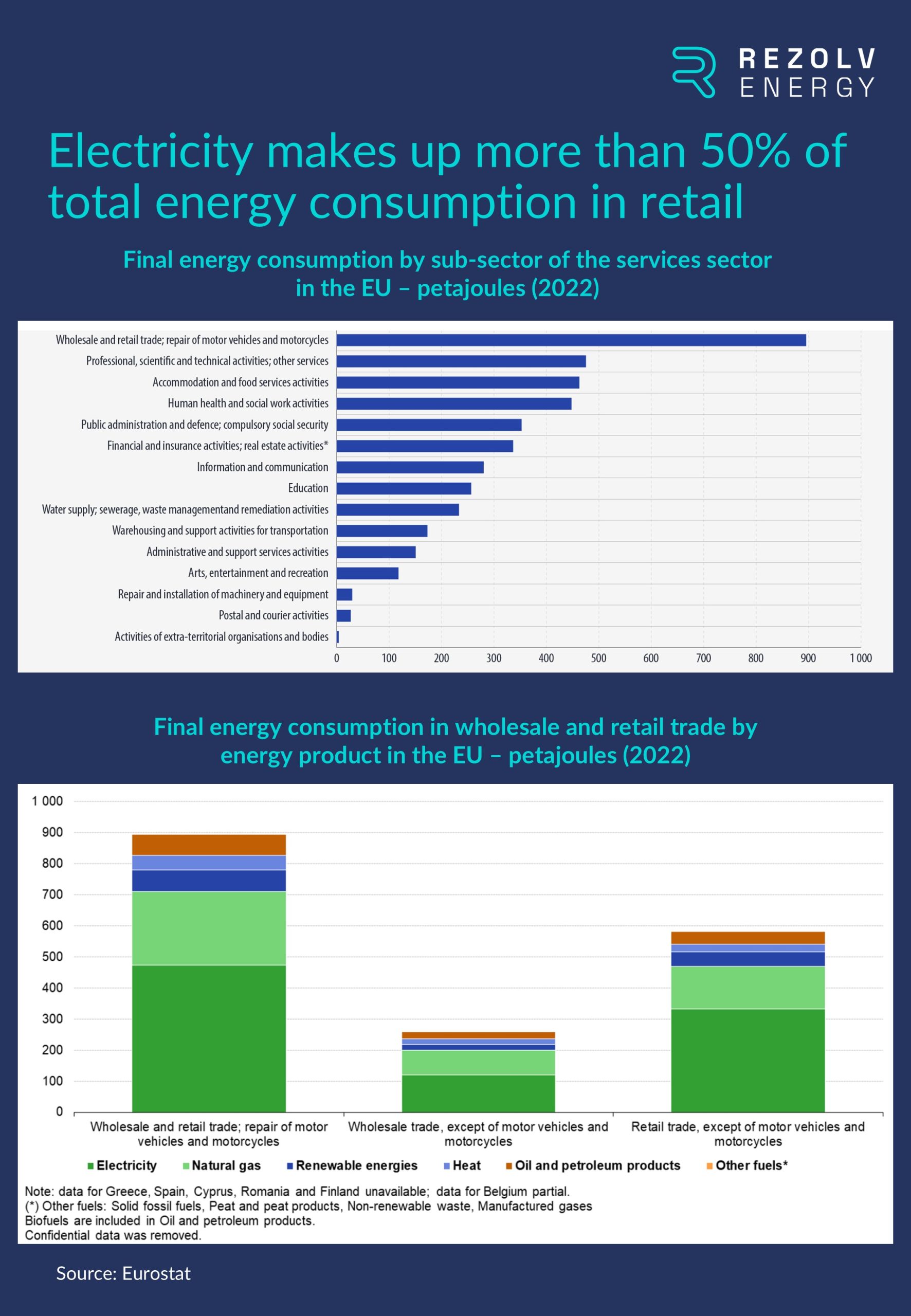

It is not a coincidence that supermarket chains dominate the list of retailers which signed the most significant PPAs last year. Supermarkets typically have a large footprint – which is one reason rooftop solar has been so popular in the sector – with ranks of fridges and freezers running 24/7. This makes supermarkets the most energy-intensive form of retail.

More specifically, retail is electricity-intensive, with electricity making up well over half of total energy consumption:

This means two things:

- Electricity consumption is a major contributor to supermarkets’ total carbon emissions (if the electricity is not coming from renewable sources)

- Supermarkets’ electricity bills can be very high indeed – a substantial component in overall operating costs. These chains are therefore particularly vulnerable to price shocks within the global energy market, and soaring bills in recent times have eaten into their margin.

We will come back to the first point. On the second point, a well-structured PPA will, in the long-term, reduce a company’s energy costs compared to traditional utility rates. There is therefore a clear commercial rationale for signing a renewable energy PPA. PPAs also offer long-term price stability, protecting companies from volatile energy markets. It is for these reasons that supermarket chains – the form of retail with the highest electricity bills – have been driving demand for PPAs within the sector.

b) European retailers are being influenced by the regulatory environment at EU level

Earlier in this series, we examined the regulations, directives and other EU initiatives which are – or will be – the most important in encouraging European companies to switch to buying more clean power. We highlighted six in particular: the Corporate Sustainability Reporting Directive (CSRD) and the European Sustainability Reporting Standards (ESRS), the Corporate Sustainability Due Diligence Directive (CSDDD), the reform of the EU’s electricity market design, the EU-wide scheme for rating the sustainability of data centres, the revised Directive on the Energy Performance of Buildings and the proposal for a Directive on Green Claims.

European retailers are impacted by nearly all of these regulations, and as the deadlines for compliance approach, so the need to switch to clean power has become more urgent.

c) Major retailers have made sustainability commitments which they now need to meet

As we saw in our previous sector deep-dives, corporations are under increasing pressure from a wide range of stakeholders – governments, investors, employees, customers etc. – to improve the environmental performance of their operations.

Retail is no exception. For example, 29 retailers are members of ‘RE100’, the global initiative which brings together businesses committed to 100% renewable electricity. Nine of these are retailers headquartered in Europe: Decathlon, Inditex (which owns Zara and Massimo Dutti, among other brands), Ingka Group (the largest IKEA franchisee holding company), BayWa, H&M, JD Sports Fashion, Next, Tesco and Zalando.

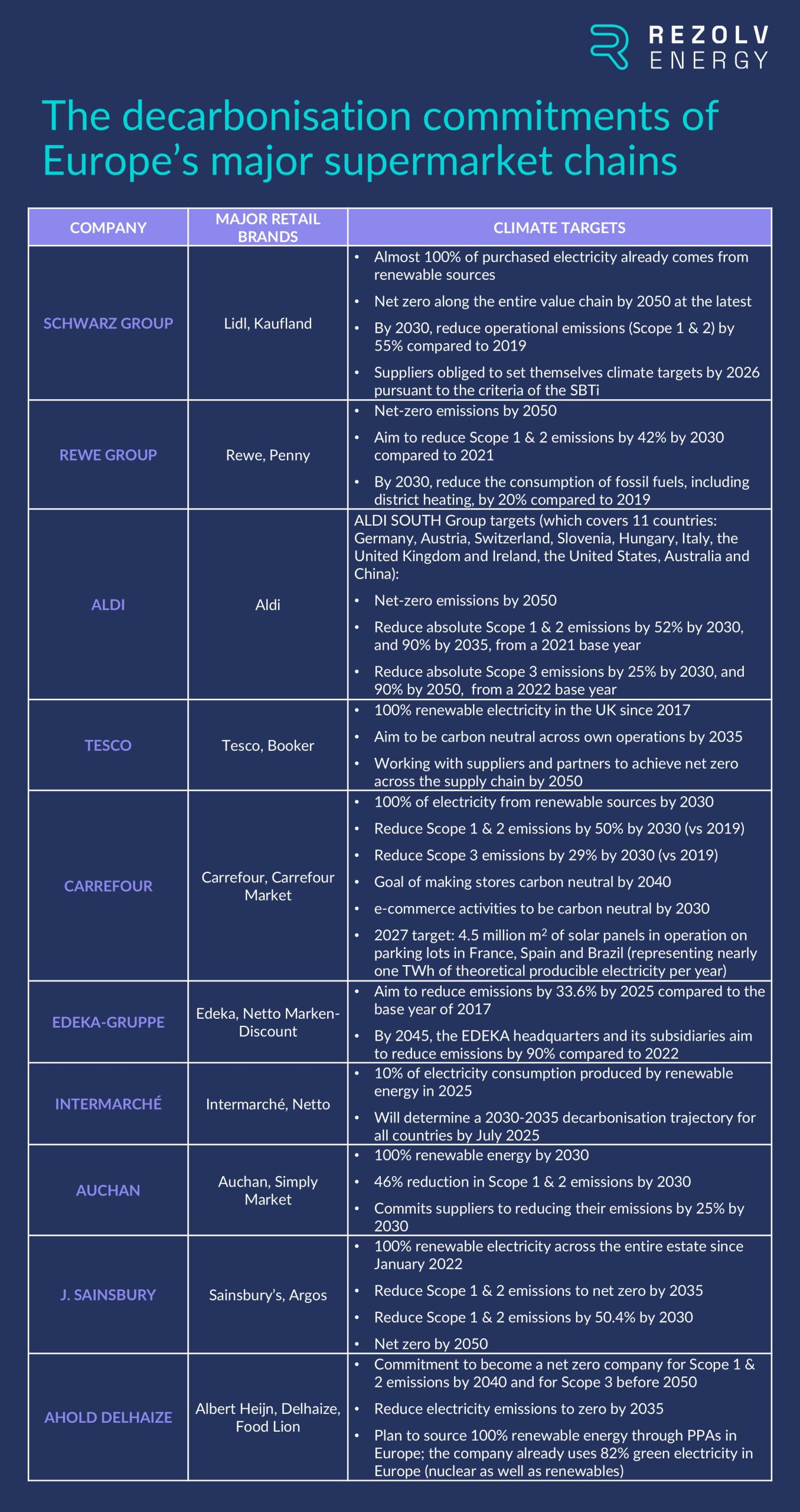

If we focus in again on Europe’s major supermarket chains, most of them have robust sustainability targets with deadlines which are approaching fast:

These three factors, then, are not specific to retail – they affect all industry sectors. There is also one additional factor which is not exactly specific to retail, but to which retailers are particularly sensitive: consumer attitudes.

Every industry must be attuned to the needs of their customers, of course, but no sector is more competitive than retail, nor is any sector more responsive to changing habits within the customer base. In retail, success or failure is determined by attention to these details, and by the speed with which companies adapt to them.

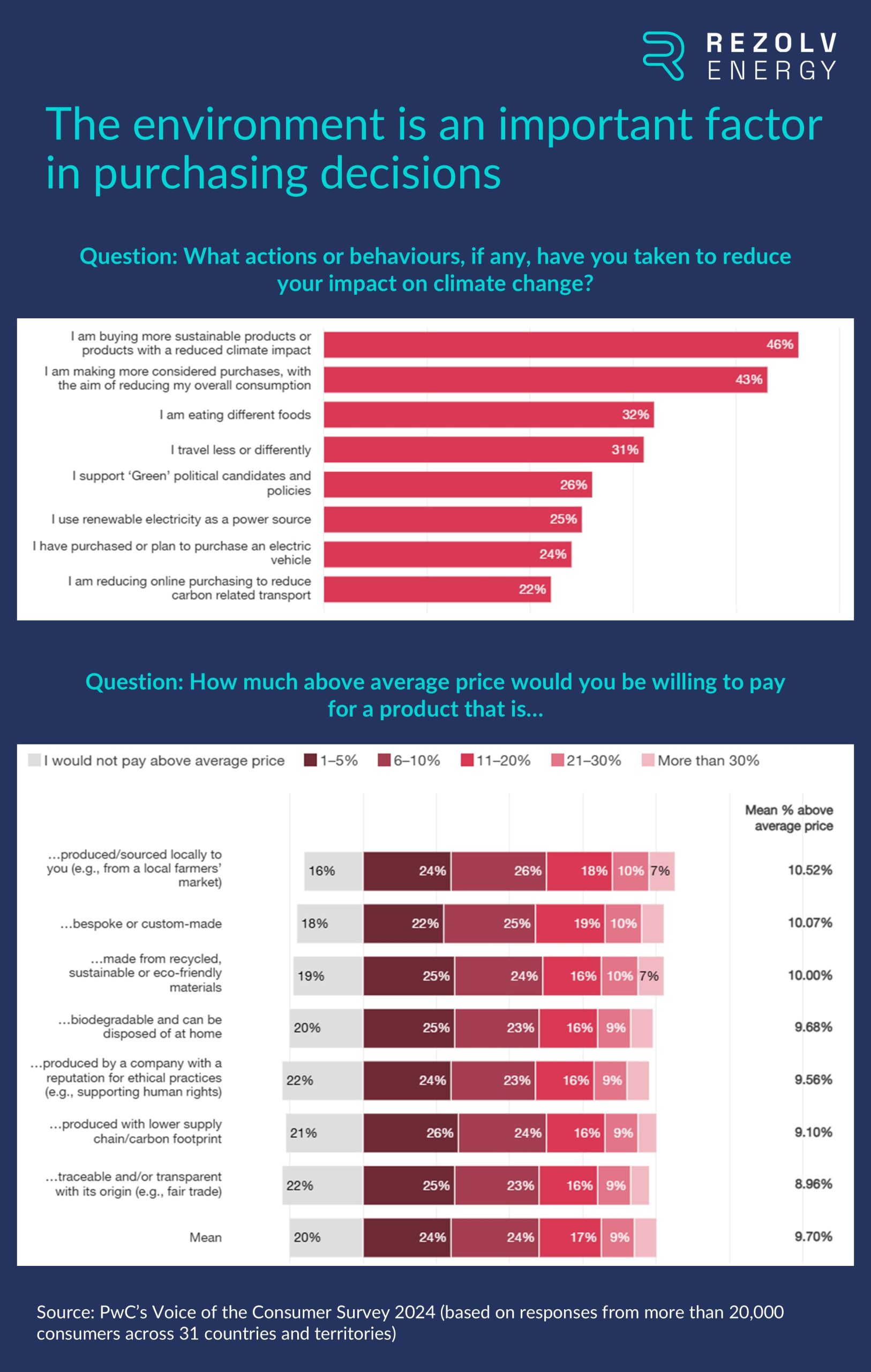

This is important in the context of renewable energy procurement because survey after survey has shown that consumers are becoming increasingly conscious of the environmental footprint of the products they buy, and of their shopping habits more broadly. This is affecting purchasing decisions, even as the costs of consumer goods have risen.

For example, PwC’s inaugural ‘Voice of the Consumer Survey’ was published in May 2024 and collected the perspectives of more than 20,000 consumers across 31 countries and territories. Almost half of the respondents (46%) said that they are buying more sustainable products as a way to reduce their personal impact on the environment. Across the board, consumers also said that they would be willing to pay 9.7% above the average price for sustainably produced or sourced goods:

These attitudes are particularly strong amongst younger shoppers, but it emphasises the link that exists between shopping habits and retailers’ approach to sustainability. Efforts to reduce emissions connect with many customers, and can therefore be a way of enhancing brand loyalty – thereby providing a vital competitive advantage.

4. What is the situation in Southeastern Europe?

Many retailers across Southeastern Europe have also started to transition across to green electricity. To give a few examples:

- IKEA: Ingka Group, the owner of most IKEA stores worldwide, has invested over €4 billion in renewable energy projects, including wind farms and solar parks. In Romania, Ingka Group acquired a 300MW solar photovoltaic project in Dâmbovița County, expected to be operational by late 2025.

- Lidl: In Romania, Lidl inaugurated a logistics centre in Fundeni, Călărași County in 2023, which was equipped with 2,650 solar panels and covered over 9,400 m2. These panels are projected to generate approximately 30% of the facility’s energy needs.

Lidl Bulgaria has solar panels on two logistics centres – in the villages of Ravno Pole and Kabile – each with a capacity of 1000 kWp, as well as at 50 of the chain’s stores across the country. All of the power produced is used for Lidl’s own needs. Last year alone, the company’s investments in the construction of PV systems exceeded 7 million leva (€3.6 million). Almost the same amount is planned for this financial year.

- Kaufland: Kaufland Bulgaria has also been proactive in installing PV systems. By March 2023, the company had activated 420 kWp of rooftop solar panels across six sites, including locations in Petrich and Sofia’s Mladost 4 district. Additionally, Kaufland Romania partnered with Enel X to implement a PV system at its logistics centre in Turda, installing over 2,000 panels to cover more than 19.3% of the facility’s annual electricity consumption.

- Billa: In October 2023, Electrohold Trade and Billa Bulgaria entered into a 10-year PPA to supply Billa with green electricity from a solar power plant. Billa has also installed solar panels on the parking lot of one of its stores in Sofia, as well as on the roof of a nearby commercial facility, together producing 20% of the store’s consumption. The system also includes 130kWh of battery storage. This year, Billa Bulgaria plans to invest 4.5 million leva (€2.3 million) in PV systems, including at the company’s new logistics centre.

- Metro: Since 2020, PV systems have been installed on the roofs of three Metro Bulgaria stores – in Blagoevgrad, Pleven and Veliko Tarnovo. Each of the solar installations there occupies an area of approximately 3,000 m2, with the energy produced covering an average of 25% of the needs of the respective store.

2025 may well be the year we start to see more retail sector PPAs in Southeastern Europe

Summing up, the strong growth in renewable energy PPAs that we have seen in the retail sector over the last two years is a result of several factors, including soaring electricity costs, regulatory pressure and the sustainability commitments many retailers have made. They have been commercial decisions aimed at avoiding volatile energy prices eating into the bottom line, with the added benefits of enhancing the ability to plan long-term and building stronger brand loyalty amongst customers.

These factors will not change, which is why the growth of renewable energy procurement in the retail sector is not a short-term trend. It is a strategic shift which is here to stay – and, as we have seen in Western Europe, expect retail to become one of the fastest-growing sectors of all when it comes to renewable energy procurement in Southeastern Europe as well.

What is coming up next time?

Earlier in this series, just under a year ago, we considered 2030 emissions targets and provided a ‘status update’ on how the countries in Central & Southeastern Europe were progressing. Our conclusion? That “the progress we have seen across the region over the last 12 months is a great start, but even more urgency is needed.”

12 months on, many of these targets have increased again and, now less than five years out from 2030, we have an even clearer sense of the situation. Next time, we will provide a revised status update on the growth of renewable energy across the region and assess whether or not countries are on track to meet their various climate goals…

Rezolv Energy secures up to €90 million in debt financing from the IFC and Raiffeisen Bank International for the St. George solar park in Bulgaria

Sofia, Bulgaria, 16 October 2024 — Rezolv Energy, an independent power producer backed by Actis, has secured up to €90 million in debt financing from the International Finance Corporation (IFC) and Raiffeisen Bank International to support the construction of the ‘St. George’ solar park in north-eastern Bulgaria.

Construction work is due to start very shortly, with the plant scheduled to come onstream next year.

This announcement follows the signing in early September of a major 12-year Virtual Power Purchase Agreement (VPPA) with Ardagh Glass Packaging-Europe (AGP-Europe), an operating business of Ardagh Group. The VPPA – one of the first to be signed in Bulgaria – is intended to provide 110 GWh per year of renewable electricity from St. George to AGP-Europe to help decarbonise its manufacturing operations across Europe.

Also in September, Rezolv confirmed that it had selected three companies to build St. George. Solarpro, a Bulgarian company, and CMC Europe will together act as the engineering, procurement and construction (EPC) partner. The high voltage work will be delivered by Green Solar Energy, another Bulgarian company.

About the St. George solar park

The 225MW St. George solar park will be built on a brownfield site: the former Silistra airport, a decommissioned airfield in north-eastern Bulgaria covering 165 hectares. The project will comprise nearly 400,000 photovoltaic panels. It will be connected to the main transmission grid via a 110kV substation and two independent connection lines totalling approximately six kilometres in length.

With an average annual power generation of more than 310 Gigawatt hours (GWh), St. George will be one of the largest solar projects in Bulgaria once it is operational next year.

In a country which has historically relied on fossil fuels for most of its energy needs, replacing fossil production with renewables delivers the maximum possible emissions reduction impact. St. George will therefore play a crucial role in Bulgaria’s energy transition and help the country meet its climate targets.

The project will create 200 new jobs in the construction phase, both people involved in light assembly – which is work suitable for men and women, on both a full-time and part-time basis – and highly-skilled engineers. Longer term, the power plant will provide local employment throughout its 30 plus years of operation.

In approving the loans, the banks acknowledged Rezolv’s commitment to sustainability, which has been built on industry best practice and aligns with international standards, including the Equator Principles and IFC’s Performance Standards on Environmental and Social Sustainability.

Alastair Hammond, CEO of Rezolv Energy, said:

“From the very start, we were all excited by the opportunity that St. George presented to take a decommissioned airfield, which has not been put to any positive use for many years, and convert it into a project to improve air quality and help Bulgaria meet its climate targets. Securing this support from the IFC and Raiffeisen Bank International is a big step towards turning that dream into a reality.”

Jaroslava Korpanec, Partner, Head of Central and Eastern Europe, Energy Infrastructure at Actis, said:

“Rezolv is showing real impetus and this latest development is yet another example of how the business is kicking into gear to accelerate the energy transition and deliver clean energy in South Eastern Europe. It’s great that lenders understand the exciting opportunity offered by the energy transition and are backing Rezolv’s projects.”

Ary Naïm, IFC Manager for Central and South Europe, said:

“Bulgaria’s transition to a sustainable energy future is crucial, and IFC’s investment in this landmark solar power project underscores our commitment to supporting this transition. By partnering with Rezolv Energy, we are fostering the development of a more diversified and sustainable energy sector in Bulgaria, enhancing energy security, and promoting environmental sustainability.”

Peter Marx, Head of Project and Structured Finance at Raiffeisen Bank International, said:

“The St. George project stands as one of the largest renewable energy initiatives in Bulgaria, marking a key step forward for the country’s energy transition. This accomplishment was only made possible by the exceptional collaboration between Rezolv Energy, the International Finance Corporation and RBI.”

Rezolv, which launched two years ago, already has well over 2GW of clean energy being prepared for construction in South Eastern Europe. As well as St. George, projects include Dama Solar in western Romania which, at 1,044MW, will be the largest solar plant anywhere in Europe once it is built. Rezolv also has more than 1GW of wind power under construction or in late stage development in Romania.

Rezolv Energy and A2A sign Virtual Power Purchase Agreement for 150 GWh of wind energy in Romania

A2A, an Italian group active in the energy, water and environment sectors, has signed a 7-year Virtual Power Purchase Agreement (VPPA) with Rezolv Energy, an independent power producer backed by Actis. The agreement provides for the purchase of 150 GWh per year of renewable energy, with the electricity generated by Rezolv’s VIFOR wind farm in Buzău County, Romania.

The renewable energy generated, which could power around 73,000 households annually, will help avoid almost 63,000 tonnes of CO2 emissions.

This is the sixth VPPA that Rezolv has signed since June. Together, the VPPAs that Rezolv has now concluded equate to 460 GWh per year – more PPA capacity than any other developer has secured in South Eastern Europe.

Once operational, VIFOR will be one of Europe’s largest onshore wind farms. Close to the Carpathian Mountains and benefiting from exceptional wind yields, Phase 1 will install 192MW in capacity with planned expansion to 461MW in phase 2. Construction is scheduled to be completed within 18 months, with VIFOR coming onstream before the end of 2025. The project is being developed by Rezolv – through its subsidiary First Looks Solutions – according to the highest international sustainability standards.

In a region which has historically relied on fossil fuels for most of its energy needs, replacing fossil production with renewables delivers the maximum possible emissions reduction impact. The project will therefore play a crucial role in the region’s energy transition and support Romania in meeting its climate targets.

Alastair Hammond, CEO of Rezolv Energy, said:

“Virtual Power Purchase Agreements are still a relatively new concept in South Eastern Europe but they are becoming an increasingly important facilitator of the energy transition. In this case, we can simultaneously contribute to decarbonisation objectives and help Romania meet its climate targets. It’s a win-win.”

Jaroslava Korpanec, Partner, Head of Central and Eastern Europe, Energy Infrastructure at Actis, commented:

“The momentum around Rezolv’s VIFOR wind farm in Romania continues with yet another VPPA signing. Once again, this demonstrates the strong demand for clean, renewable energy that exists in the C&I market as businesses look to decarbonise and meet their net zero targets. Congratulations to the Rezolv team for getting these agreements over the line while powering on with the development of its projects.”

Rezolv Energy was launched 18 months ago by Actis, a leading global investor in sustainable infrastructure, and already has well over 2GW of clean energy being prepared for construction in Southeastern Europe. As well as the VIFOR wind farm, projects include Dama Solar in western Romania which, at 1,044MW, will be the largest solar plant anywhere in Europe once it is built, the 600MW Dunarea East & West Wind Farms in Romania’s Constanța County, and St. George, a 229MW solar project in north-eastern Bulgaria.

ICT companies should act now to secure the green power needed for data centre growth

In the last article in this series, we explored the regulations, directives and other EU initiatives which are – or will be – the most important in encouraging European companies to switch to buying more renewable power. One of the pieces of legislation highlighted was a new delegated regulation on the first phase for establishing an EU-wide scheme to rate the sustainability of EU data centres, which was adopted in March 2024. The regulation establishes a European database for operators of data centres with an installed IT power demand of at least 500 kW, and requires those operators to report on various KPIs by 15 September 2024 – and then by 15 May in 2025 and subsequent years.

The regulation is very important for the telecoms industry, which we considered earlier in this series, and even more so for the subject of this article: the information & communications technology (ICT) sector. In this piece, we will explore why the ICT industry – and the growth of data centres specifically – is so significant for the development of renewable energy in Central and South Eastern Europe, and therefore to Rezolv’s mission in the region:

- How does the ICT sector compare with other industry sectors when it comes to renewable energy procurement?

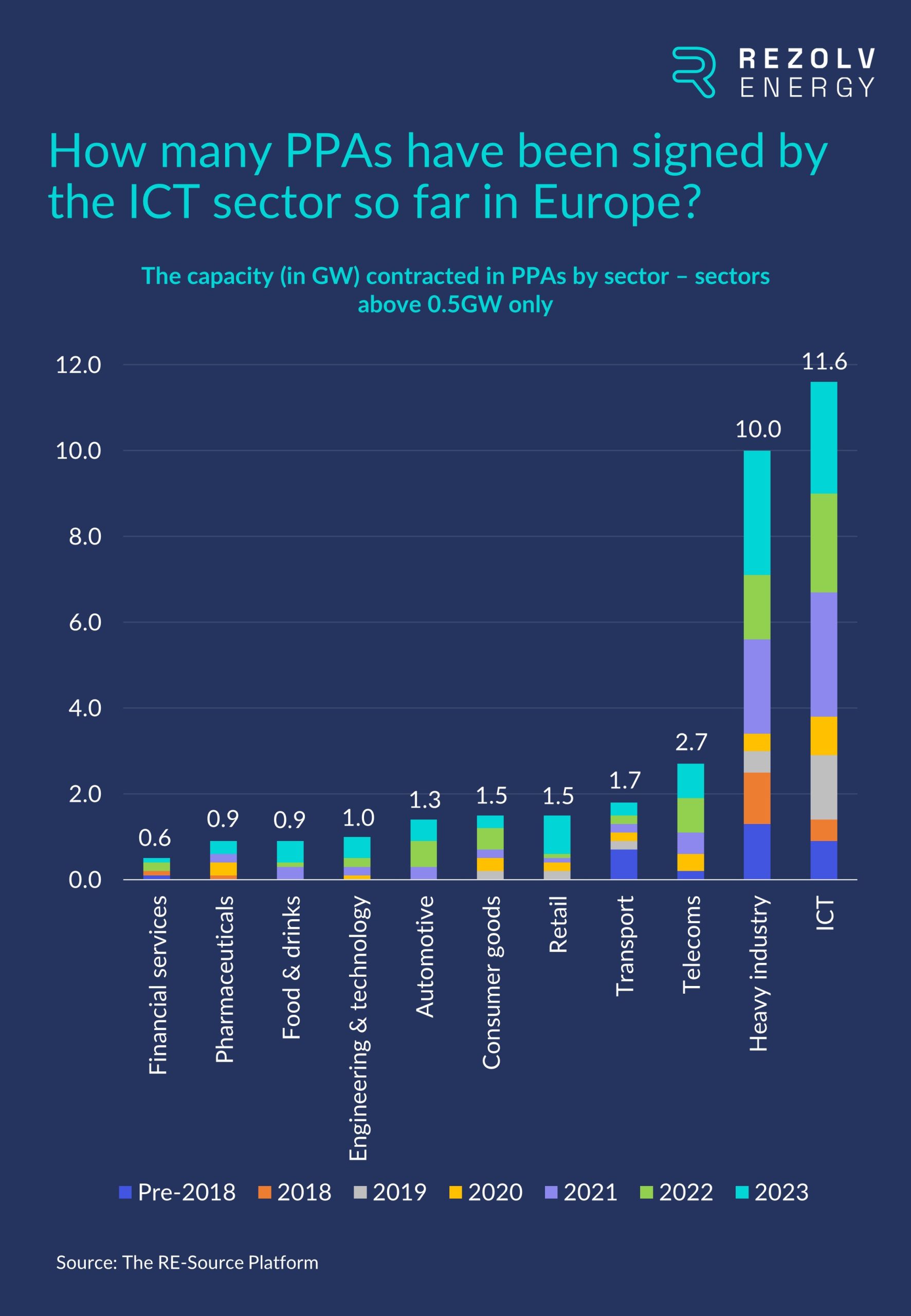

The ICT industry was leading the way on renewable energy purchasing in Europe well before the EU-wide scheme to rate the sustainability of EU data centres was on the agenda. Indeed, across Europe, ICT companies have contracted more than four times the amount of green energy capacity through Power Purchase Agreements (PPAs) than any other sector apart from Heavy Industry:

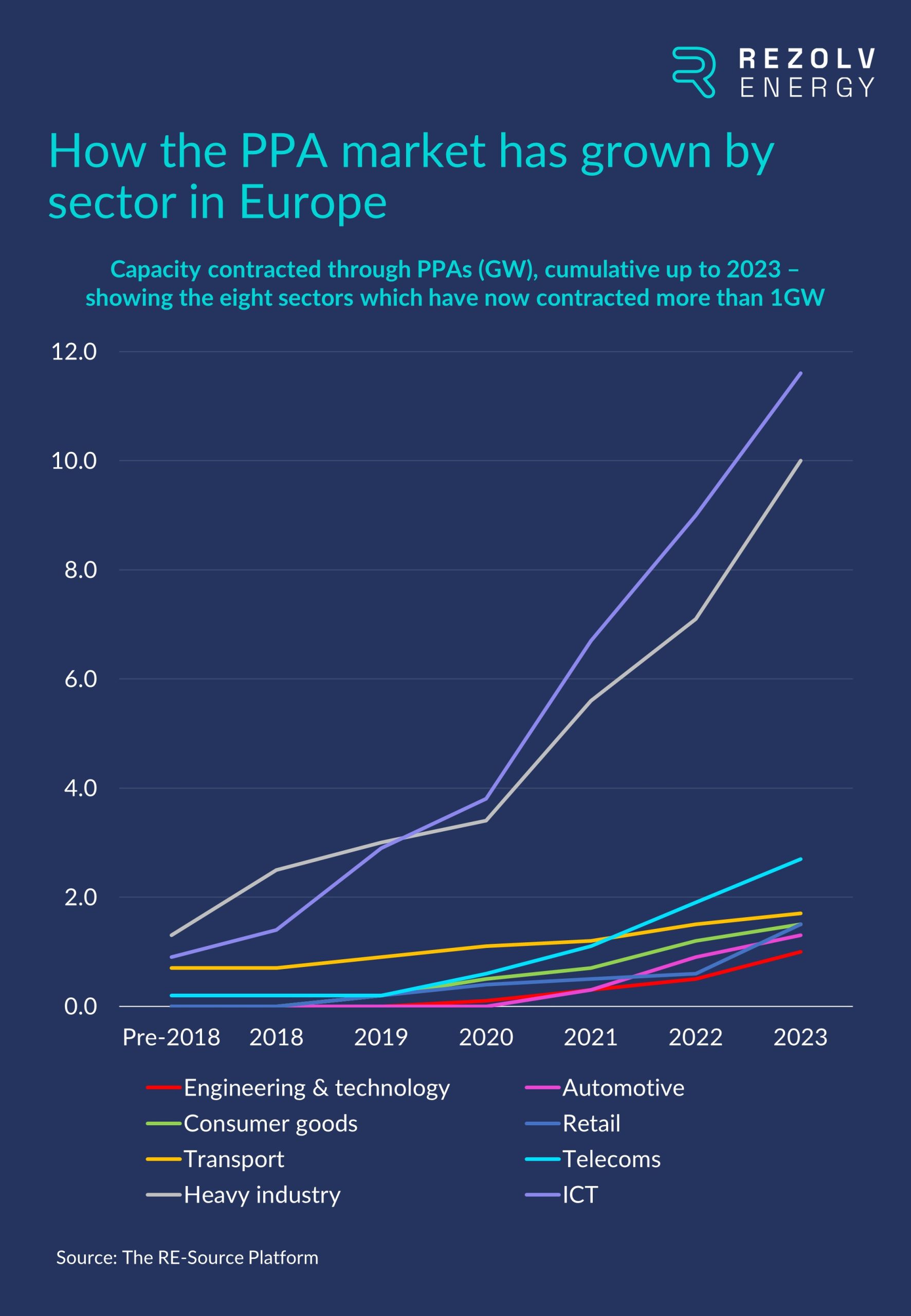

Heavy Industry was actually a slightly earlier adopter of the PPA model than ICT, but ICT moved ahead in 2019 and has stretched its lead since then:

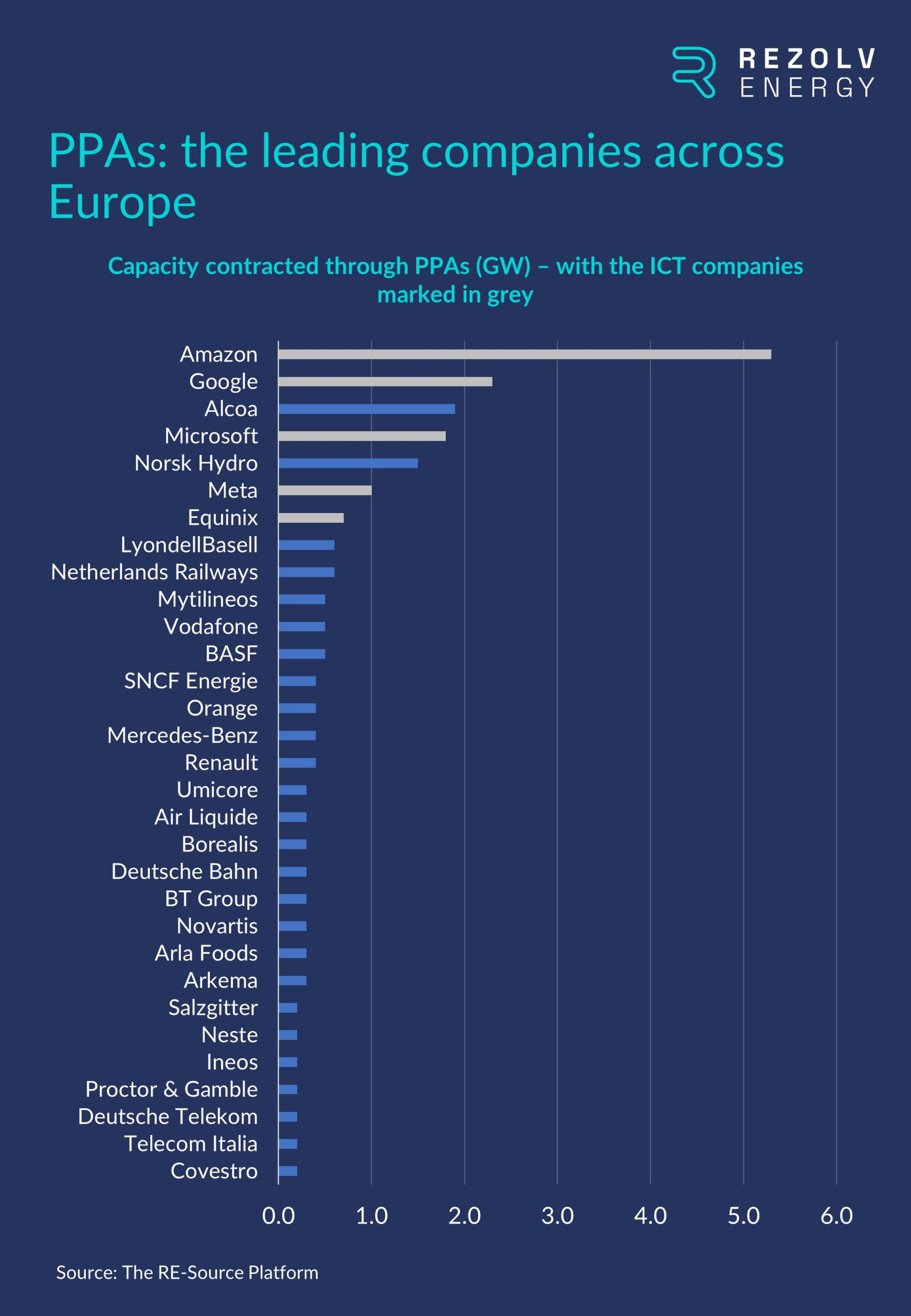

2. Which ICT companies are leading the way on PPAs in Europe?

More than any other sector, the ICT industry’s track record of signing PPA deals is dominated by a relatively small number of companies. When you consider the list of companies which have contracted the largest amount of capacity through PPAs in Europe, there are five ICT companies in the top seven: four of the traditional ‘Big Five’ tech companies (Amazon, Google, Microsoft and Meta) plus Equinix, the only business outside the ‘Big Five’ which breaks into the list of top five data centre companies worldwide:

3. Overall, how much progress has each of these companies made when it comes to renewable energy procurement?

Compared to many other industries, these five companies all have very strong track records when it comes to renewable energy purchasing:

- Amazon: In 2019, Amazon set a goal to match 100% of the electricity it used with renewable energy by 2030. This goal was achieved in 2023, seven years early. Last year, BloombergNEF named Amazon the world’s largest corporate purchaser of renewable energy for the fourth year in a row, buying more solar and wind power than the next three companies combined. In that 12-month period, Amazon announced 74 individual PPAs across 16 different markets, totalling 8.8GW of capacity. Overall, this brought Amazon’s announced corporate PPA portfolio to 33.6GW.

- Google: In 2017, Google matched 100% of its annual electricity consumption globally with renewable energy for the first time. It has gone on to repeat that feat every year since, with the company contracting 1GW through PPAs last year.

- Microsoft: In 2023, Microsoft increased its contracted portfolio of renewable energy assets to more than 19.8GW, including projects in 21 countries, and signed new PPAs in Brazil, the US, New Zealand and Poland. In FY23, the company’s total renewable electricity use stood at 23.6 million MWh, and it aims to reach 100% renewable energy next year.

- Meta: As of 2020, Meta’s global operations have been supported by 100% renewable energy. Globally, the company was second on the list of renewable energy buyers in 2023, announcing 3GW of PPAs.

- Equinix: In 2023, Equinix maintained 96% renewable energy coverage across its global footprint, its sixth consecutive year of 90%+ renewable energy coverage. The company’s goal to achieve 100% renewable energy coverage by 2030.

- Given how much progress has already been made by the world’s largest ICT companies, is there much scope for continued growth in the volume of renewable energy purchased?

The answer to this question is a resounding ‘yes’.

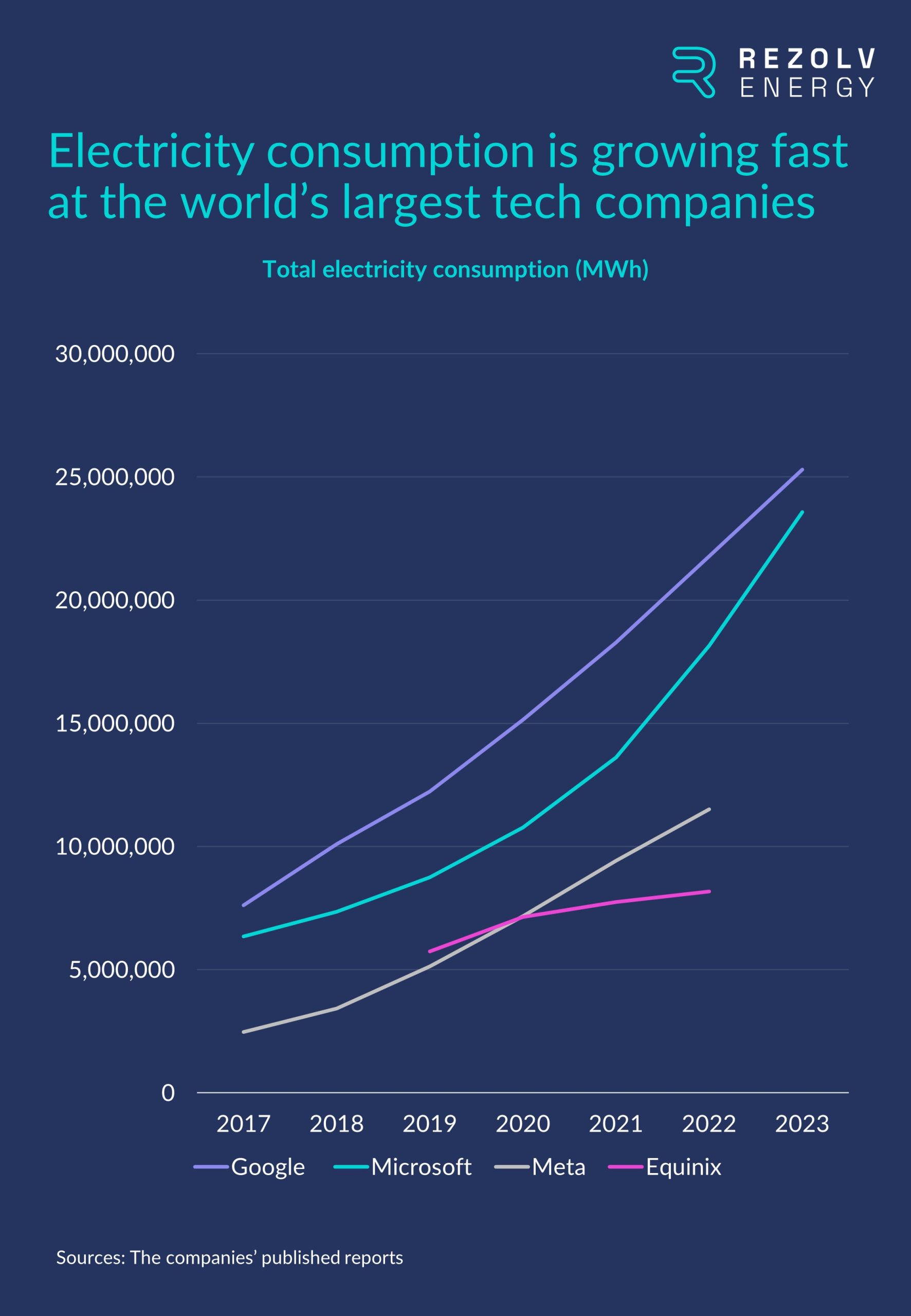

The issue for all of these businesses is that maintaining such high levels of renewable energy coverage will be incredibly challenging given their rising electricity consumption. The chart below considers four of these companies – Google, Microsoft, Meta and Equinix – and provides an indication of the scale of the task:

The primary issue is the rapid growth in the volume of data that these companies are processing. For example, electricity consumption in Meta’s data centres was 97% of the company’s total electricity consumption in 2022. More data requires ever higher computational power, and scaling up processing capacities in data centres requires more electricity. As the International Energy Agency (IEA) has clarified, the extra electricity is required not only for additional equipment such as servers, but also for cooling to deal with the immense heat build-up from data processing.

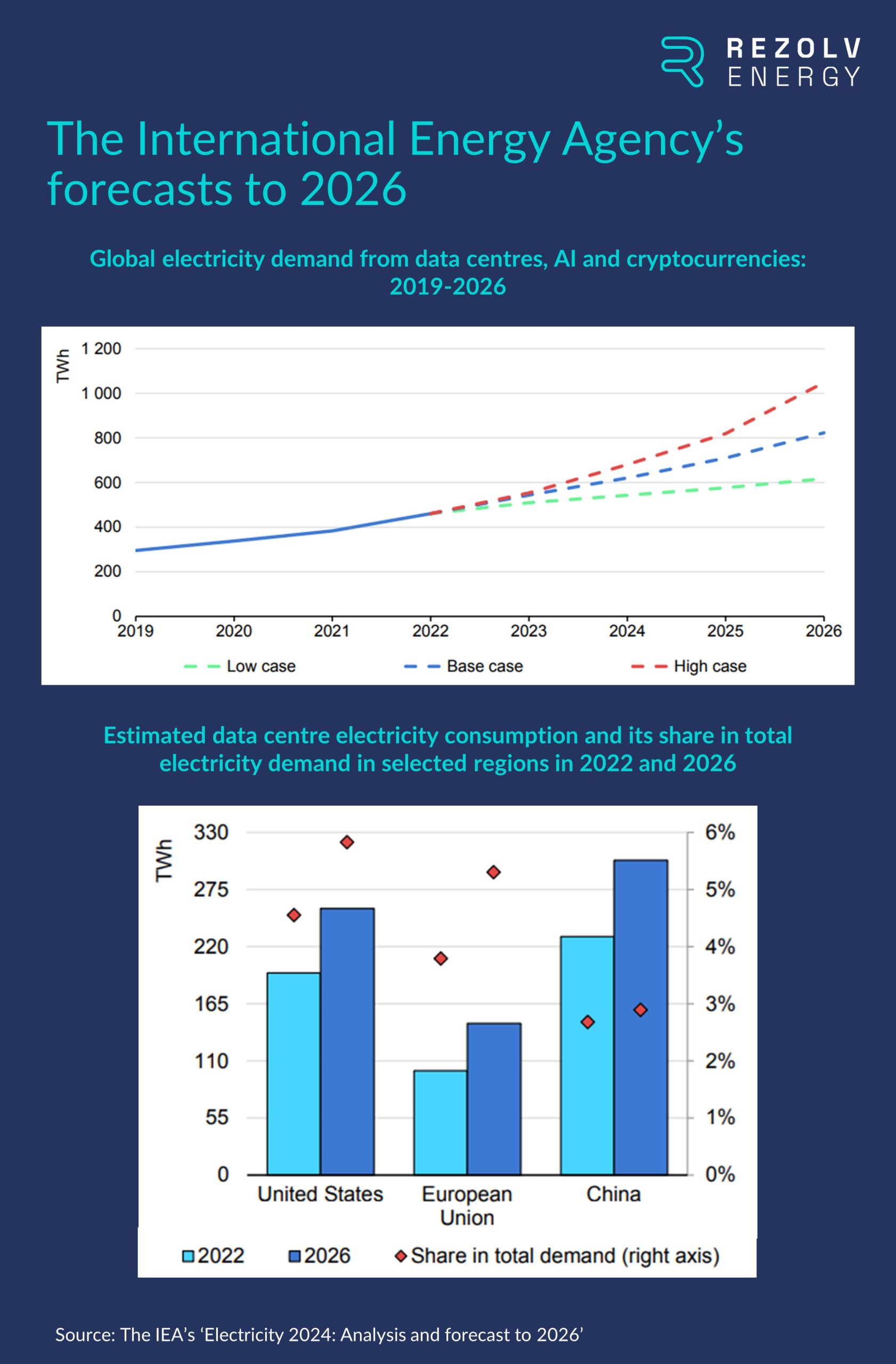

The concern now is that the additional computational power needed for the rapid growth of Artificial Intelligence models and their applications will only accelerate the already soaring electricity demand. On average, a ChatGPT query requires nearly 10 times as much electricity to process as a Google search, and the IEA estimated earlier this year that electricity consumption from data centres, AI and the cryptocurrency sector could double by 2026. Having consumed an estimated 460 TWh in 2022, the IEA forecasts that data centres’ total electricity consumption could reach more than 1,000 TWh in 2026, roughly equivalent to the electricity consumption of Japan:

This, of course, has major implications for the Big Tech companies’ sustainability targets as well.

For example, in July, Google revealed that its greenhouse gas emissions had climbed 48% over the past five years (and 13% between 2022 and 2023), blaming electricity consumption from data centres and supply chain emissions as the primary cause of the increase. The company admitted that its goal of reaching net zero emissions by 2030 “won’t be easy” and confirmed that there was now “significant uncertainty” about its ability to reach that target.

Microsoft also admitted in May this year that energy use related to its data centres was endangering its “moonshot” target of being carbon negative by 2030. Brad Smith, Microsoft’s President, said that “the moon has moved” due to the company’s AI strategy.

5. Are there other factors which will encourage further renewable energy procurement in the ICT sector?

If we retain our focus on the Big Tech companies, there is one other important factor which will also drive more corporate PPAs. Earlier in this series, we considered the impact of companies committing to net zero across the entire production chain – so covering Scope 3 emissions as well as Scope 1 (emissions occurring from sources that are controlled or owned by the company) and Scope 2 (indirect emissions associated with the purchase of power).

Of the companies we have been considering so far, we have already mentioned Microsoft’s pledge to be carbon negative by 2030 and Google’s target to achieve net-zero emissions across its value chain by 2030. Google has also implemented a ‘Google Renewable Energy Addendum’ that asks its largest hardware manufacturing suppliers to commit to achieving a 100% renewable energy match by 2029.

Meta has the same 2030 target as Google, and Equinix has committed to achieving a 50% reduction in Scope 3 emissions from fuel and energy-related activities by 2030.

Amazon aims to be net-zero carbon by 2040 and, based on the company’s most recent sustainability report, has “identified a list of the highest-emitting suppliers directly supporting our operations, and expect those suppliers, who collectively contribute more than 50% of emissions globally to Amazon’s Scope 3 footprint, to provide a plan for how they will decarbonize their operations and demonstrate real progress over time. We will prioritize our business toward those who provide their plans and results on their path to net zero carbon emissions.”

Over time, this pressure on suppliers from multinational companies with comprehensive net zero commitments will also become an important driver of PPAs in Europe.

6. Will this affect Central and South Eastern Europe significantly?

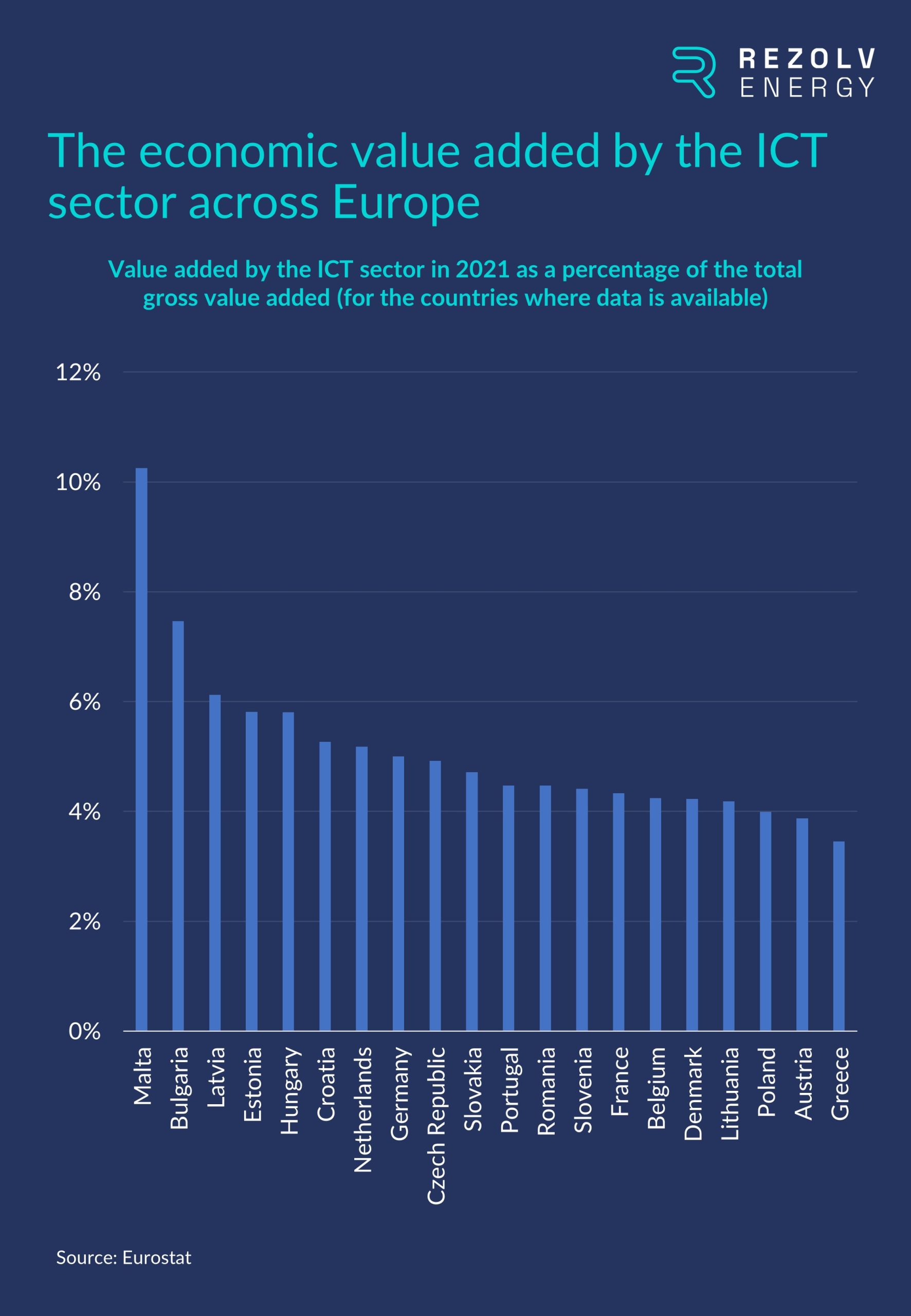

These trends are not restricted to the handful of very large companies at the very top of the ICT industry – they are being felt right across the sector and are impacting much smaller companies too. This matters for Central and South Eastern Europe because ICT is a very significant industry for many countries in this region. To assess this, it’s useful to consider the EU member states where the ICT sector adds the most value economically:

The data is not complete for every country, but based on these numbers, there is no obvious divide between Western Europe and Central / Eastern Europe when it comes to the importance of the ICT sector. In fact, of the seven countries where the ICT industry contributes more than 5% of the total value added, five are from CEE: Bulgaria, Latvia, Estonia, Hungary and Croatia.

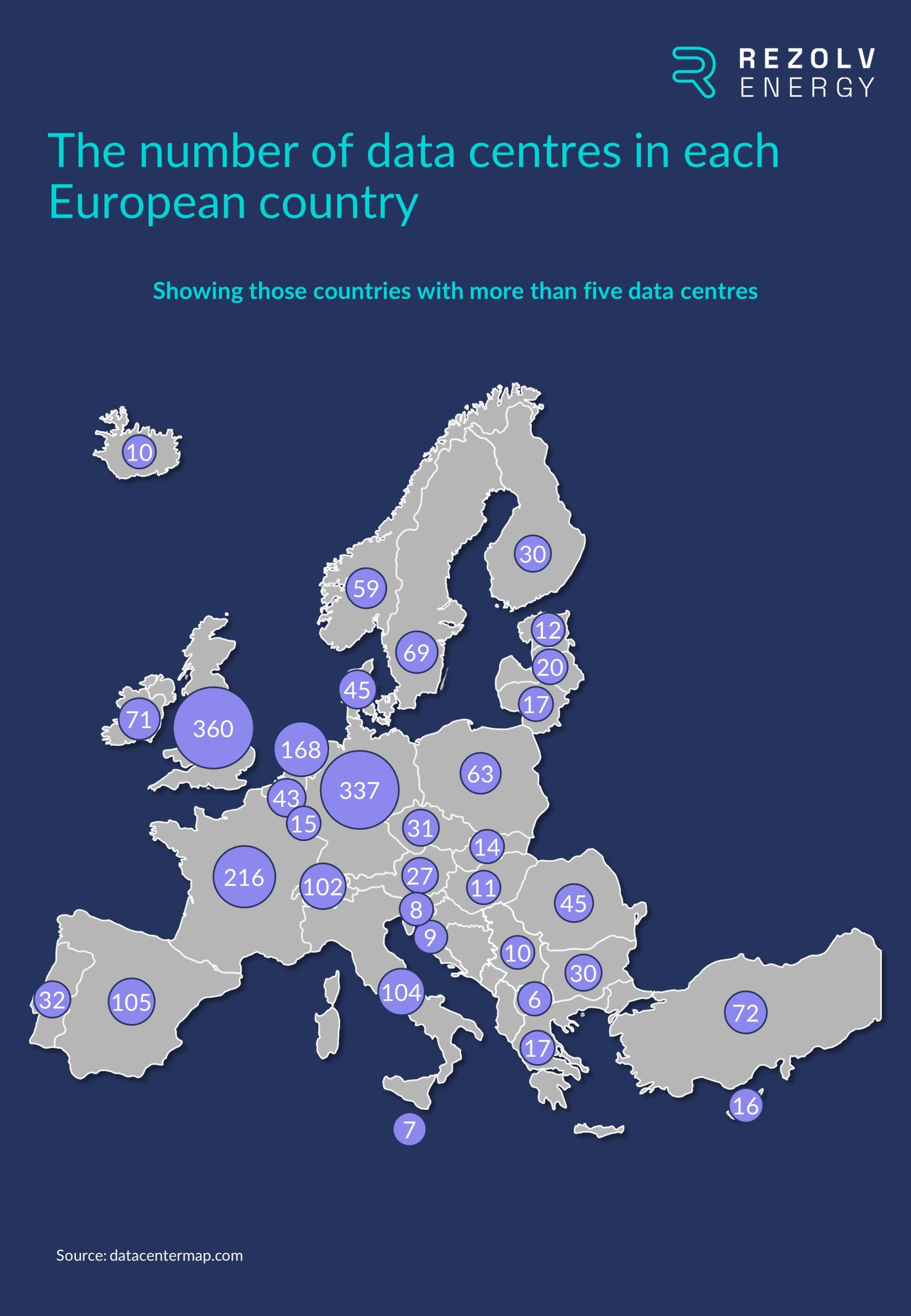

There is a bigger geographical split when it comes to the number of data centres situated across Europe. The most developed Western European countries host the largest number of data centres, but there are still significant numbers in CEE:

This is a fast-moving space, though, and things could change very quickly. For example, in mid-July, the Romanian government and Google signed a memorandum of understanding on cooperation projects in “digital infrastructure, innovation and research”. The announcement did not provide specific details about Google’s plans in Romania, but it did mention Romania’s attractiveness for data centre projects and local press reports have indicated that Google is in negotiations to invest $2 billion in developing data centres in the country.

It is also important to note that, as has been proved by Rezolv’s recent deals with T-Mobile Czech Republic, Slovak Telekom, CE Colo Czech Republic, Bekaert and Ardagh Glass Packaging-Europe, the virtual PPA (VPPA) model has removed national borders as a barrier to renewable energy procurement within the EU.

In contrast to a physical PPA which require the buyer and producer to be in the same country, or in neighbouring countries with connected grids, a VPPA is a financial arrangement where the buyer receives certificates verifying that the energy has come from a specific renewable source, with the clean power being fed into the grid.

This means that even if a tech company’s electricity demand is concentrated in Western Europe, the door is open for them to benefit from the renewable energy boom that is underway in South Eastern Europe and procure clean power from a project (or projects) in this region.

Summing up: there is no time to lose

ICT companies should act now to ensure they are first in line for green power.

This starts with understanding the power usage efficiency of data centre providers and alternative suppliers, but it will also drive interest in green PPAs, including in Central and South Eastern Europe.

What is coming up next time?

Next time, we will be looking at another important, if slightly lower-profile, industry sector when it comes to green PPAs: retail…

Ardagh Glass Packaging-Europe enters Bulgarian renewable energy market by signing Virtual Power Purchase Agreement with Rezolv Energy

Ardagh Glass Packaging-Europe (AGP-Europe), an operating business of Ardagh Group, announced today that it has entered a long-term Virtual Power Purchase Agreement (VPPA) with Rezolv Energy’s St. George solar photovoltaic (PV) project in Bulgaria, securing renewable electricity for its glass manufacturing operations across Europe from April 2026.

Schneider Electric, a leading adviser in corporate renewable energy procurement and carbon management, supported AGP-Europe in the VPPA negotiation.

The VPPA – one of the first to be signed in Bulgaria – is intended to provide 110 GWh per year of renewable electricity to AGP-Europe, over 12 years. It complements AGP-Europe’s renewable energy supply from wind power, secured in Sweden earlier this year. Together, thanks to their different sources, they are designed to provide AGP-Europe with a consistent renewable power supply throughout the year.

In conjunction with other Power Purchase Agreements in its portfolio, this deal is designed to enable AGP-Europe to meet over 80% of its 2030 renewable electricity targets.

Rezolv is able to sign this VPPA in Bulgaria, with a major international industrial firm, because Bulgaria is a full member of the Association of Issuing Bodies (AIB) and going through the final steps to connect to the AIB Hub, thus making its Guarantees of Origin tradeable across Europe. Adopting this essential European legislation and enacting it fully directly supports Bulgaria in decarbonising its electricity grid for the benefit of everyone.

About the St. George solar park

The St. George solar park will be built on a brownfield site: the former Silistra airport, a decommissioned airfield covering 165 hectares. The project will comprise nearly 400,000 photovoltaic panels. St. George will be one of the largest solar projects in Bulgaria once it is operational in the summer of 2025.

In a country which has historically relied on fossil fuels for most of its energy needs, replacing fossil production with renewables delivers the maximum possible emissions reduction impact. St. George will therefore play a crucial role in Bulgaria’s energy transition and help the country meet its climate targets.

The project will also be developed to the highest international sustainability standards to ensure that it leaves a lasting, positive legacy.

Martin Petersson, CEO AGP-Europe said:

“We are pleased to have finalised this agreement in just six months, which is largely due to Rezolv’s flexibility, the support and technical know-how of Schneider Electric, and our own experience in this field.”

“The Bulgarian solar project perfectly meets our aim to diversify the locations of our renewable energy supply and to support emerging energy markets: AGP-Europe benefits from a supply of renewable electricity, while helping Bulgaria’s transition to low-carbon energy.”

Alastair Hammond, CEO, Rezolv Energy added:

“By signing this VPPA, AGP-Europe has become one of the most important corporate investors in Bulgaria’s energy transition. Through it, the company has become the leading enabler of St. George, a 229 MW solar project which, overall, will deliver an average of 313 Gigawatt hours of renewable electricity annually. AGP-Europe is therefore making a direct contribution to reducing Bulgaria’s dependence on fossil fuels and to enhancing its energy security.”

Jaroslava Korpanec, Partner, Head of Central and Eastern Europe, Energy Infrastructure at Actis, commented:

“In signing this VPPA for its solar project in Bulgaria, Rezolv Energy is placing itself at the heart of pioneering practices to drive the energy transition across Central and Eastern Europe while helping leading businesses power their operations more sustainably through renewable energy.”

Rezolv Energy was launched 18 months ago by Actis, a leading global investor in sustainable infrastructure, and already has well over 2GW of clean energy being prepared for construction in South Eastern Europe. As well as St. George, projects include Dama Solar in western Romania which, at 1,044MW, will be the largest solar plant anywhere in Europe once it is built. Rezolv also has more than 1GW of wind power under construction or in late stage development in Romania through two projects it is developing in partnership with Low Carbon.

Rezolv Energy hands contracts to three companies, including Solarpro and CMC Europe, to build the ‘St. George’ solar park in Bulgaria

Actis-backed Rezolv Energy has selected three companies – CMC Europe, Solarpro and Green Solar Energy – to build the 229MW ‘St. George’ solar park in Silistra Municipality in Northeastern Bulgaria. Construction work is due to start very shortly, with the plant coming onstream next year.

CMC Europe, and Eastern Europe’s leading technology integrator Solarpro, will together act as the engineering, procurement and construction (EPC) partner for the project.

St. George will be connected to the main transmission grid via a 110kV substation and two independent connection lines totalling approximately six kilometres in length. The high voltage work will be delivered by Green Solar Energy, also a Bulgarian company.

About the St. George solar park

The St. George solar park will be built on a brownfield site: the former Silistra airport, a decommissioned airfield covering 165 hectares. The project will comprise nearly 400,000 solar panels.

In a country which has historically relied on fossil fuels for most of its energy needs, replacing fossil production with renewables delivers the maximum possible emissions reduction impact. St. George will therefore play a crucial role in Bulgaria’s energy transition and help the country meet its climate targets.

The power produced will be sold to commercial and industrial users through long-term Power Purchase Agreements (PPAs). The first PPA for St. George is set to be announced very soon – a major deal and one of the first PPAs to be signed in Bulgaria. It follows the five pioneering PPAs that Rezolv has signed in recent months connected to its 461MW ‘VIFOR’ wind farm in Romania.

As well as PPAs, St. George will be financed through loan facilities from a consortium of international lending partners and regional commercial lenders.

CMC Europe and Solarpro’s role as EPC partner will involve working alongside Rezolv to implement the Environmental and Social Action Plan for St. George. The Environmental and Social Action Plan is consistent with Rezolv’s sustainability strategy, which has been built on industry best practice and aligns with international standards, including the Equator Principles and the International Finance Corporation (IFC)’s Performance Standards on Environmental and Social Sustainability.

In the construction phase of the project, up to 200 people will be hired, with as many employees as possible coming from the local area. Training and skills development programmes are also being put in place. This is a priority, because closing the skills gap in the renewables industry is a crucial part of the energy transition in Bulgaria. Longer term, St. George will continue to provide local employment throughout its 30 plus years of operation.

Alastair Hammond, CEO, Rezolv Energy, said:

“St. George will be one of the largest solar projects in Bulgaria, so it was necessary to find the right blend of local experience and international expertise. We also needed partners with outstanding track records who shared our commitment to sustainability. CMC Europe, Solarpro and Green Solar Energy meet all of those requirements.”

Jaroslava Korpanec, Partner, Head of Central and Eastern Europe, Energy Infrastructure at Actis, said:

“It’s terrific to see Rezolv Energy moving forward with the St. George solar park in Bulgaria. Once developed, St. George will be one of the largest solar plants in Bulgaria, operating 229MW of solar energy and playing a decisive part in the country’s energy transition. With both the VIFOR wind farm and St. George solar farm progressing strongly, Rezolv has the wind in its sails and is positioned to make a real difference in the region.”

Rezolv, which launched 18 months ago, already has well over 2GW of clean energy being prepared for construction in South Eastern Europe. As well as St. George, projects include Dama Solar in western Romania which, at 1,044MW, will be the largest solar plant anywhere in Europe once it is built. Rezolv also has more than 1GW of wind power under construction or in late stage development in Romania.